Click

for the financial advice if you like (I won't) …. Despite that

these finance guys do have their fingers on the pulse

Europe

Can and Will Cause a Systemic Collapse… Are You Ready?

25

July, 2012

A

lot has been said about the European Crisis. I’m going to explain

it all in simple terms.

In

simple terms, today we are facing a Crisis that is far, far worse

than 2008. Before it ends, it is quite possible that we will see the

entire Western Financial System collapse and a new system put into

place.

This

will mean:

1)

Many major banks disappearing, as well as numerous potentially

lengthy bank holidays (think Argentina in 2001)

2)

Multiple sovereign defaults as well as broad economic contractions

and their commensurate unemployment/ civil unrest/ erasure of

retirement accounts/ pensions (this process has already begun in some

US municipals, e.g. San Bernandino and Stockton California as well as

Harrisburg Pennsylvania).

3)

Possibly new currencies being introduced or new denominations of

currencies (say one new unit being worth 1,000 of the old one)

4)

Massive wealth destruction to the tune of tens of trillions of

Dollars (think MF Global i.e. the money is gone…

only systemically… in fact we just had another such instance with

PF)

5)

A global contraction that will result in new political/ power

structures being implemented as well as the breakup of various

countries/ unions.

6)

Very serious trade wars to begin (see Obama’s recent attack on

China) and very possibly a real war.

If

the above make you frightened, you’re not alone. As I’ve dug

deeper and deeper into the inner workings of the global financial

system over the past months, the information I’ve come across has

only gotten worse. I’ve been holding off writing all of this

because up until roughly April/May it seemed possible that the

world mightveer

towards another outcome.

I

no longer view this to be the case. I am almost certain that what

I’ve written above will come to pass. I know that much of what I’ve

written to you in the past could be labeled as “gloom and doom.”

However, I want you to know that I do not use the words “systemic

collapse” lightly.

Indeed, I wish I wasn’t mentioning them now, but I’d be doing you

a disservice not to bring them up because we’re well on our way

towards it.

So

buckle up and let’s dive in.

In

order to understand why we’re at risk of the financial system

collapsing, you first need to understand how the global banking

system works. When you or I buy an asset (say a house, or shares in a

stock, or a Treasury bond), we do so because we’re looking to

increase our wealth through either capital gains or through the

income that asset will pay us in exchange for us parking our capital

there.

In

simple terms, you’re putting/ lending your money somewhere

(especially if you’re buying a bond) in the hope of increasing the

value or your money.

This

is not how banks work. When a bank buys something, especially a bond,

it parks that bond on its balance sheet as an “asset.” It then

lends money out againstthat

asset. This in of itself is not problematic except for the fact that

the financial modeling of 99% of banks base assume that sovereign

bonds are “risk-free.” Put another way, these models assume that

the banks will always get

their money back on 100 cents on the Dollar.

Yes,

you read that correctly, despite the fact that world history is

replete with examples of sovereign defaults (in the last 20 years

alone we’ve seen more than 15 including countries as significant as

Russia, Argentina, and Brazil), most banks assume that the sovereign

bonds sitting on their balance sheets are risk free.

This

phenomenon occurs worldwide, but given that it will be Europe, not

the US that takes the system down, I’m going to focus on European

bank models/ capital ratios.

You

may or may not be familiar with EU banking law. EU banks are meant to

comply with Basel II which is a series of capital requirements and

other specifications meant to limit systemic risk.

In

terms of capital ratios, Basel II requires that EU banks have equity

and Tier 1 capital equal to 6% of risk

weighted assets.

On paper this idea was supposed to

limit bank leverage to 16 to 1 (the bank has €1 in capital or

equity for every €16 in loans).

However,

the term “risk weighted assets” destroys this premise because it

means that the bank’s loan portfolio and ultimately

its leverage ratio are

based on the bank’s in

house models/

assumptions concerning the risk

of its loans.

Let

me give you an example…

Let’s

say XYZ Bank lends out €50 million to a corporation. The bank won’t

necessarily claim that all €50 million is “at risk.” Instead,

the bank will claim that only a percentage of this €50 million is

“at risk” based on the company’s credit rating, financial

records (debt to equity, etc), and the like.

Thus,

based on “in-house” risk modeling, European banks could in fact

lend out much, much more than the Basel II requirements would imply.

Considering that both bank profits and executive

compensation were/are closely tied to more lenient definitions of

“risk-weighted,” (i.e. lend as much as you possibly can) it’s

safe to assume that EU banks are in fact much, much more leveraged.

Indeed,

according to the IMF’s “official” analysis, EU banks as a whole

are leveraged at 26 to 1. I would argue that in reality many of them

are well north of 30 to 1 and possibly even up to 50 or 100 to 1.

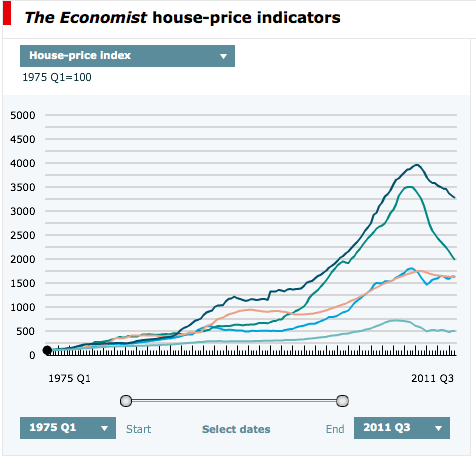

The

reason I can claim this with relative certainty is because the EU

housing bubbles dwarfed that of the US. In the chart below the US

housing bubble is the lowest line. After it comes Britain (blue) and

Italy (orange) then Ireland (green) and finally Spain (dark blue).

You

can only get bubbles of this magnitude if you’re lending to

literallyanyone with

a pulse. And you can only lend that much if your in-house risk models

believe that the risk of lending to anyone with

a pulse is much, much lower than reality.

You

can only get bubbles of this magnitude if you’re lending to

literallyanyone with

a pulse. And you can only lend that much if your in-house risk models

believe that the risk of lending to anyone with

a pulse is much, much lower than reality.

Hench,

EU banks are likely leveraged at much, much more than 26 to 1.

Indeed, considering how leveraged and toxic US banks’ (especially

the investment banks’) balance sheets became from the US housing

bubble, the above chart should giveeveryone pause

when they consider the TRUE state of EU bank balance sheets.

This

fact in of itself makes the possibility of a systemic collapse of the

EU banking system relatively high.

With

that in mind, I’ve begun positioning subscribers of my Private

Wealth Advisory for

the next leg down in the markets. We’ve already locked in over 30

winning trades this year by finding “out of the way” investments

few investors know about and timing our positions to benefit from the

various developments in Europe and the global economy. When

you combine this with our 2011 track record, we’ve had 72 straight

winners and not one closed loser since July 2011.

Indeed,

we just locked our 72nd winner yesterday: a 9% gain in less than a

month

To

learn more about Private

Wealth Advisory and

how it can help you get through the EU Crisis with gains… NOT

pains…

Best

Regards,

Graham

Summers

Chief Market Strategist

Phoenix Capital Research

Chief Market Strategist

Phoenix Capital Research

No comments:

Post a Comment

Note: only a member of this blog may post a comment.